🛡️ Term Insurance: Everything You Should Know (Simplified)

✅ 1. Best Tenure

-

Take term insurance till age 60–65.

-

Why? You’ll achieve your financial goals by then.

-

Don’t pay extra premium for cover till 80–90.

✅ 2. When Is It Necessary?

-

If your family depends on you, or you have a home loan, get insured!

-

Take a term plan of 20X your annual income.

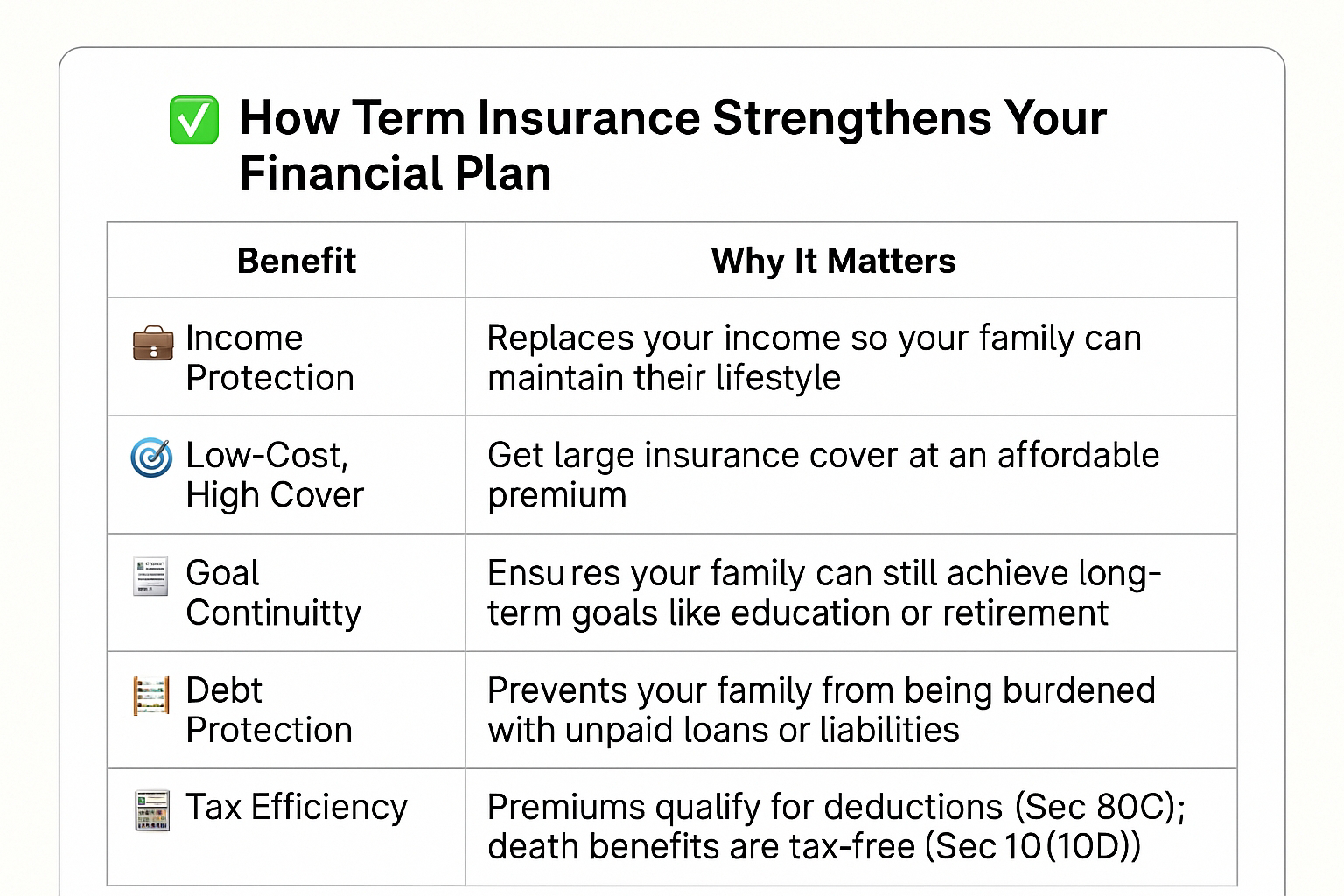

✅ 3. What Should It Cover?

-

All loans and liabilities.

-

Sustain your family’s current lifestyle.

-

Beat inflation over time.

✅ 4. Life Changes? Update Your Cover

-

After marriage, childbirth, or new loan, increase your life cover.

✅ 5. Cheapest & Purest Life Insurance

-

Term insurance is the only life policy you should buy.

-

It’s low-cost and high-coverage.

✅ 6. Tax Tip

-

If you're investing more than ₹1 lakh/year (e.g., ELSS), take term insurance to complete your 80C deduction.

✅ 7. Don’t Worry About Wasted Premium

-

You don’t regret car insurance if you don’t crash—same with term insurance.

-

Life is unpredictable.

✅ 8. SIP to Pay Premiums

-

Set up a monthly SIP in a liquid fund to accumulate premium easily.

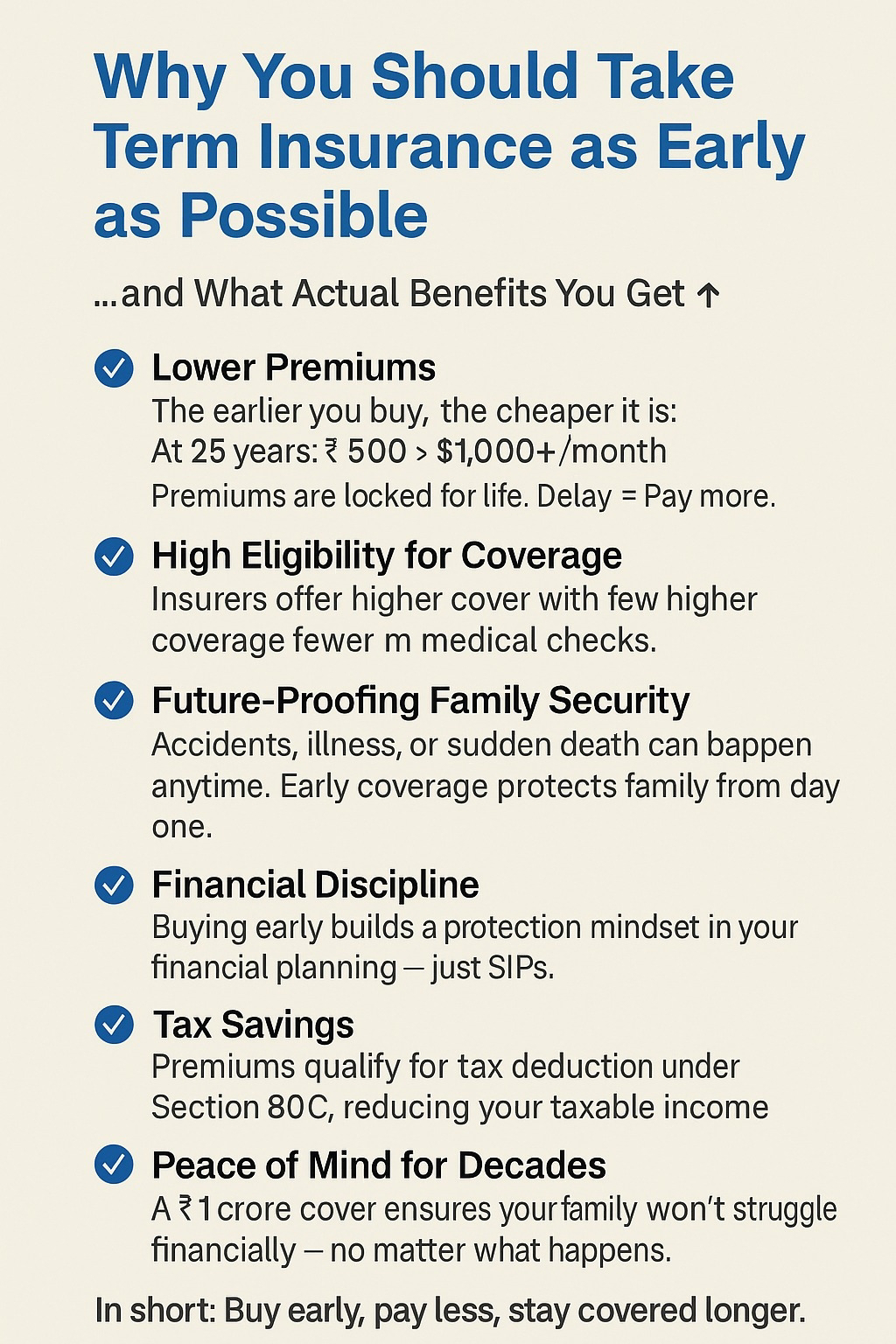

✅ 9. Take It Early, Pay Less

-

Premiums are locked when you buy early.

-

Delay = Higher premium.

✅ 10. Keep Insurance & Investment Separate

-

Don't mix them (e.g., ULIPs).

-

Higher premium + risk of policy lapse.

✅ 11. Use Mutual Funds for Long-Term Goals

-

Don’t extend term plan beyond 65. Invest extra in mutual funds.

🧐 Choosing the Right Term Plan

Company Must Be:

-

Big, reputed, trustworthy.

-

High Claim Settlement Ratio (CSR).

-

Strong AUM (Assets Under Management).

-

Check IRDAI reports — stick to top 5 insurers.

➕ Optional Riders (Add-Ons)

-

Critical Illness Rider

-

Lump sum payout on diagnosis of major illness (check exclusions).

-

-

Accidental Disability Rider

-

Pre-decided amount for partial/full disability after an accident.

-

-

Zero-Cost Term Plan

-

Return your premiums at 60 if no longer needed.

-

❌ What to Avoid

-

❌ Return of Premium Plans (Too expensive)

-

❌ Limited Pay Options (Invest extra in mutual funds)

-

❌ Monthly Payout to Family (Better to take lump sum)

✅ How to Avoid Claim Rejection

-

Always disclose smoking, drinking, illnesses.

-

Medical checkup is a must.

-

Keep records filed safely.

⚠️ Bonus Tip

-

Many insurance claims go unclaimed.

-

Use an advisor who can help your family navigate after you.