🛡️ टर्म इंश्योरेंस: आपकी वित्तीय योजना का एक ज़रूरी हिस्सा

टर्म इंश्योरेंस आपके परिवार की आर्थिक सुरक्षा और जोखिम प्रबंधन में मदद करता है। यह अनपेक्षित परिस्थितियों, जैसे आपकी असमय मृत्यु, में आपके परिवार की आर्थिक मदद करता है।

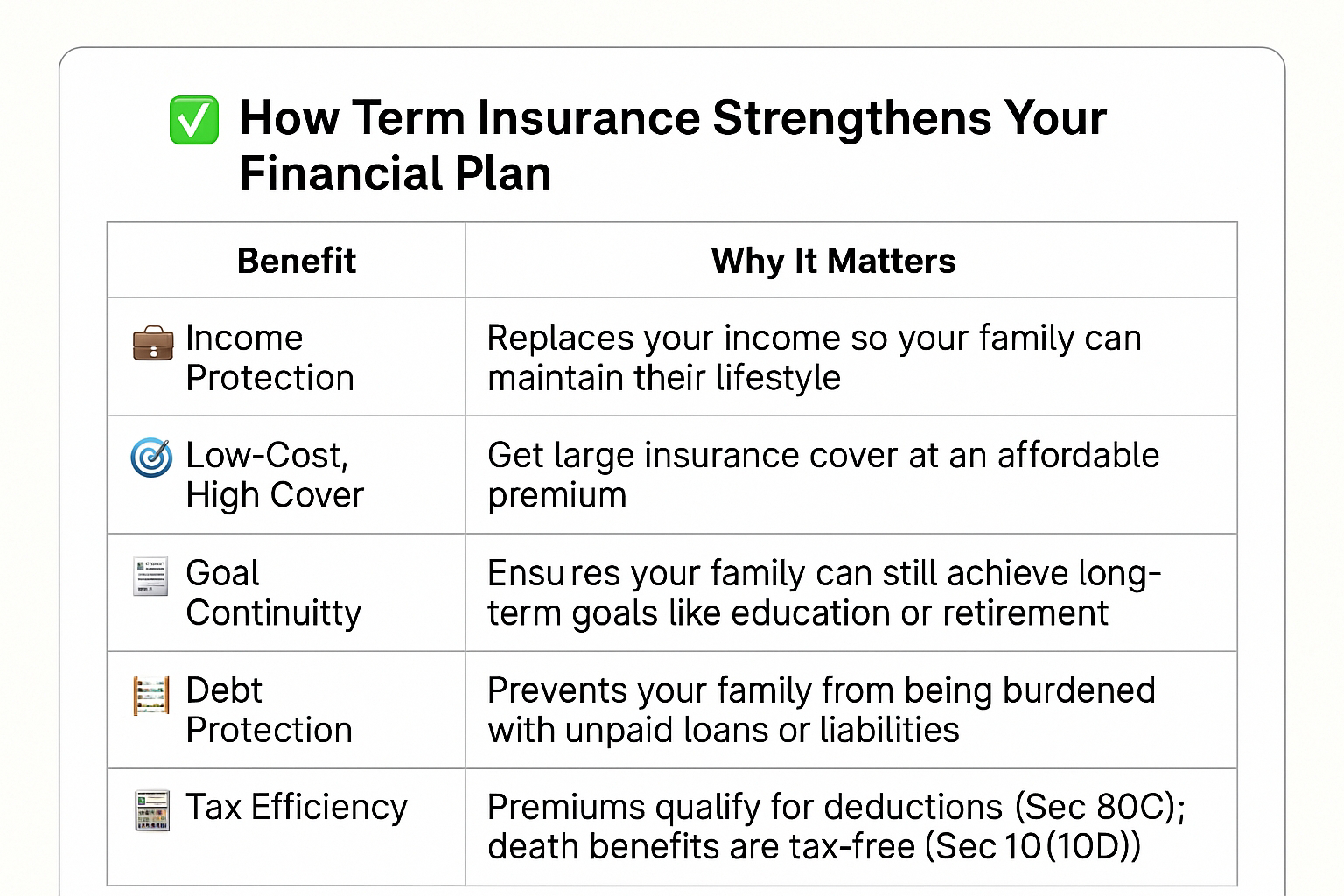

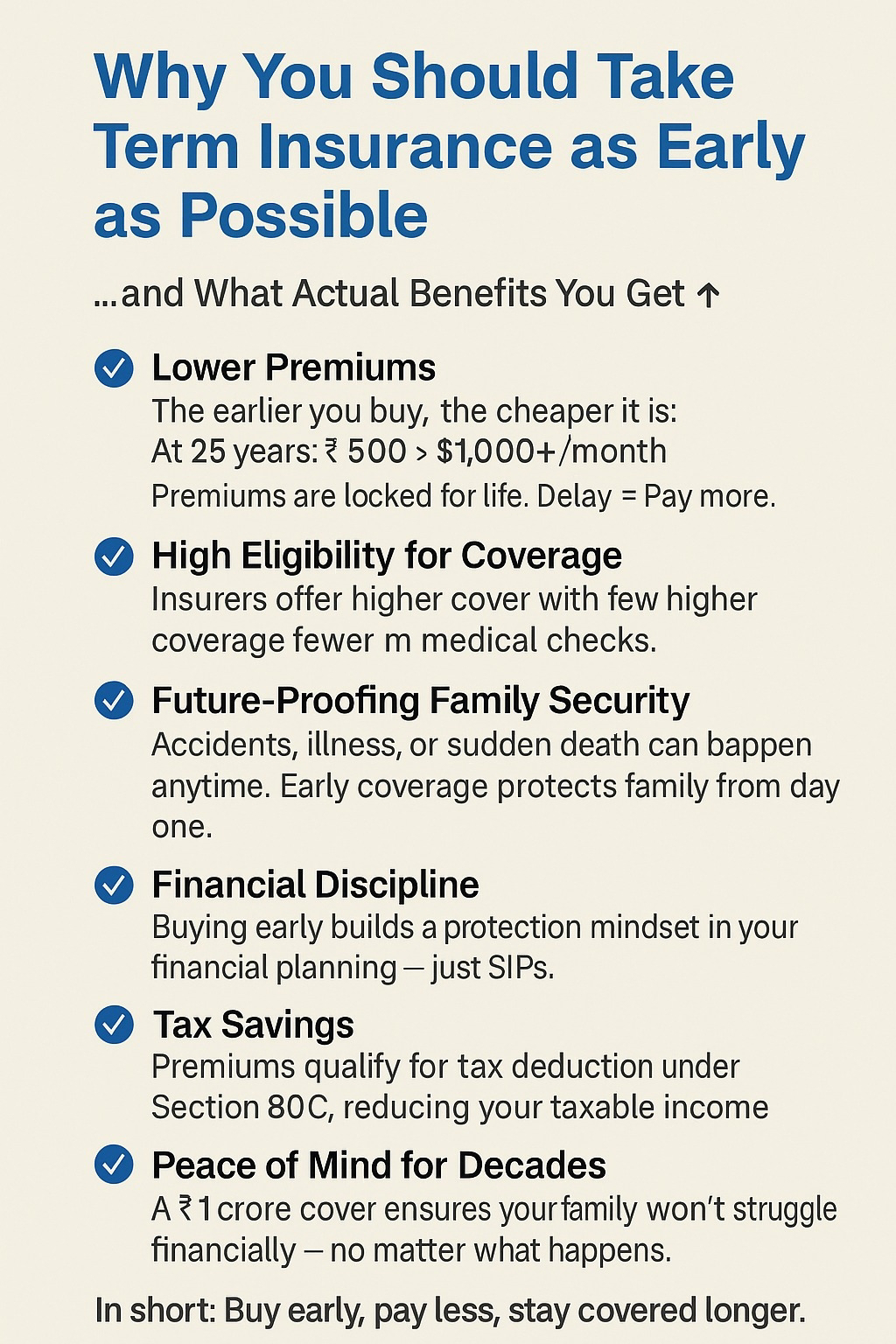

💼 1. आय की सुरक्षा (Income Protection)

- अगर आप परिवार के कमाने वाले सदस्य हैं, तो आपकी आमदनी पर पूरा परिवार निर्भर करता है।

- टर्म इंश्योरेंस आपकी मृत्यु की स्थिति में उस आमदनी को रिप्लेस करता है।

- इससे आपके परिवार का रहन-सहन, बच्चों की पढ़ाई और रोज़मर्रा की ज़रूरतें पूरी होती रहती हैं।

💸 2. कम प्रीमियम में ज़्यादा सुरक्षा (Low-Cost, High Coverage)

- टर्म प्लान बहुत ही कम प्रीमियम में उच्च बीमा राशि प्रदान करते हैं (जैसे ₹50 लाख से ₹1 करोड़ या उससे अधिक)।

- इससे आप बिना ज़्यादा खर्च किए अपने परिवार को आर्थिक रूप से सुरक्षित कर सकते हैं।

🎯 3. लंबी अवधि के लक्ष्यों की सुरक्षा (Protects Long-Term Goals)

- आपकी अनुपस्थिति में भी यह सुनिश्चित करता है कि परिवार के लक्ष्य पूरे हो सकें, जैसे:

- बच्चों की शिक्षा या शादी

- होम लोन की अदायगी

- जीवनसाथी का रिटायरमेंट

🧾 4. ऋण सुरक्षा (Debt Protection)

- अगर आपके ऊपर कोई लोन है (जैसे होम लोन, पर्सनल लोन), तो टर्म इंश्योरेंस यह सुनिश्चित करता है कि आपके परिवार को वह बोझ न उठाना पड़े।

🧮 5. कर लाभ (Tax Benefits - धारा 80C और 10(10D))

- टर्म इंश्योरेंस के लिए दिए गए प्रीमियम पर आपको धारा 80C के तहत टैक्स में छूट मिलती है।

- मृत्यु लाभ पर मिलने वाली राशि धारा 10(10D) के अंतर्गत पूरी तरह टैक्स फ्री होती है।

📊 सारांश: क्यों टर्म इंश्योरेंस ज़रूरी है?

| लाभ | विवरण |

|---|---|

| ✅ आय की सुरक्षा | परिवार की आमदनी सुनिश्चित करता है |

| ✅ कम प्रीमियम, अधिक सुरक्षा | कम खर्च में ज़्यादा बीमा |

| ✅ लक्ष्य पूरे होते रहें | परिवार के सपने रुकें नहीं |

| ✅ कर्ज से मुक्ति | लोन का बोझ परिवार पर न पड़े |

| ✅ टैक्स बचत | प्रीमियम पर छूट और क्लेम पर टैक्स नहीं |